Cost Accounting

Precise cost analysis that supports decisions and improves performance

What is

Cost Accounting?

Cost accounting is one of the branches of management accounting, aimed at enabling an organization to determine the results of its operations over a defined period. It focuses on recording the full, aggregate production costs across the company by compiling data on cost elements drawn from various documents and notices relating to material usage costs, labor costs, and the costs of purchasing or producing the services needed for different business activities.

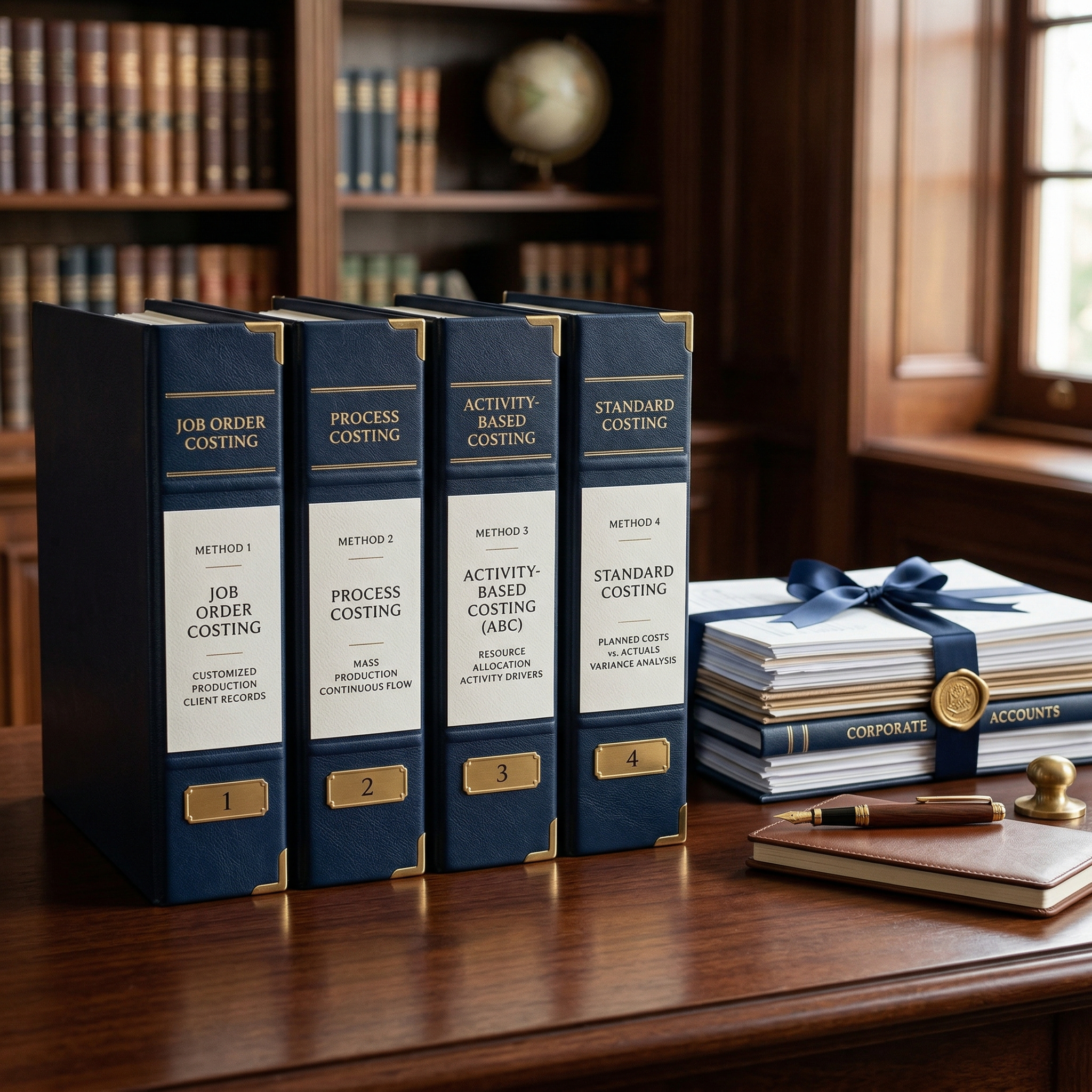

Types of Cost Accounting

Cost accounting includes several main methods used by organizations depending on the nature of their activity and their financial analysis objectives.

Activity-based costing: tracks resource consumption and allocates costs to activities and products more precisely than traditional methods, helping to understand the cost of each product or service more accurately.

Standard costing: sets a predetermined cost for each production unit (the standard cost), then compares it to the actual cost to identify variances and analyze their causes, helping to control and improve costs.

Flexible budgeting: prepares budgets that reflect changing costs as activity or production levels change, offering flexibility in financial planning and helping evaluate performance more effectively.

Marginal costing: focuses only on the variable costs of a product and is used to calculate the contribution margin (revenue minus variable costs). It is used in decisions such as pricing or accepting special orders.